The digitalization of tax operations is a process that must necessarily be pursued but making sure that it is in line with the tax authorities. Specifically, tax authorities are the ones who enable the development and actual implementation of evolutionary processes in this field. Due to the pandemic, digital has become an increasingly integral and inseparable part of the life of companies, which more than ever have to be ready for new changes.

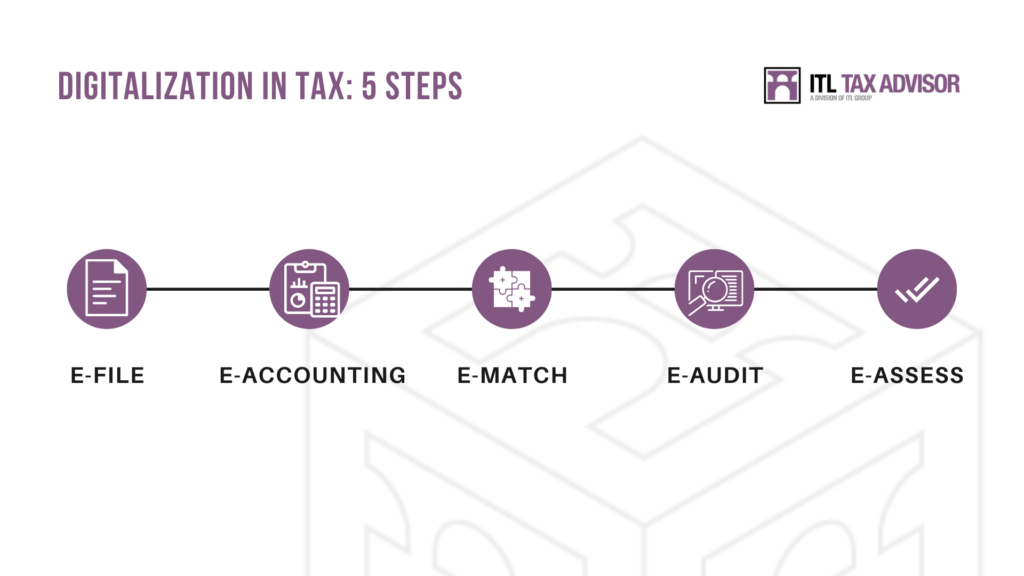

Five levels of digitalization: E-file, E-accounting, E-match, E-audit ed E-assess.

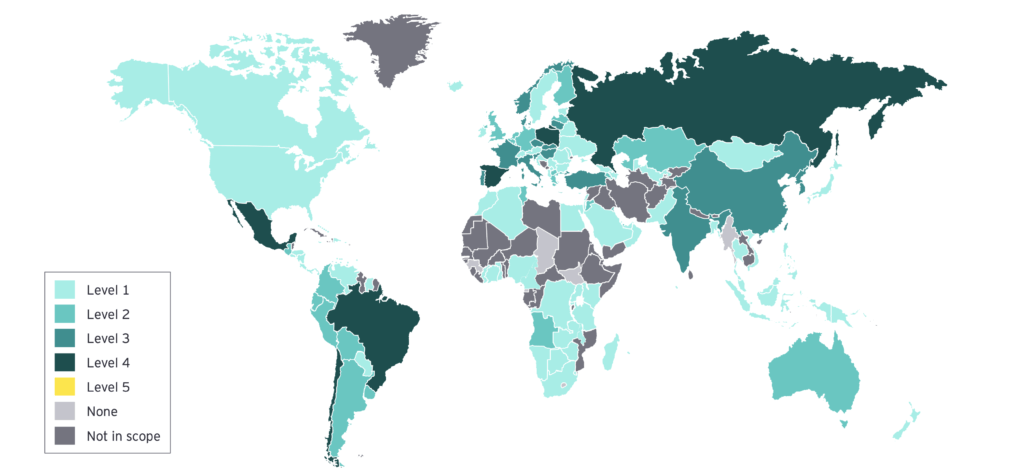

Digital tax administration can be understood through the maturity model, which presents 5 levels of development regarding the evolution of tax management with the use of technological tools and processes.

1. The first level is called E-file: it is a “basic” stage, in which one finds the use of a standardized electronic form for compulsory or optional tax returns; in addition, other income data (e.g. payroll, financial) compiled electronically and matched annually.

2. The second level, E-accounting, involves submitting accounting data or other data sources to support the compilation (e.g. invoices, trial balance) in a defined electronic format according to a defined schedule; in this level, we see frequent additions and changes.

3. Next we find E-match, a level in which Hungary is currently, along with other European countries: submission of additional accounting and source data; the government accesses additional data (bank statements), starts comparing data across tax types, and potentially across taxpayers and jurisdictions in real-time.

4. The fourth level, E-audit, is the next step for Hungary, what we are moving towards. It involves the analysis of data by government agencies, which is then cross-referenced to real-time fills to map the geographic, economic ecosystem; taxpayers receive electronic audit assessments with a limited turnaround time on their transactions. Russia is currently at this stage.

5. The fifth and final level of evolution of digital tax administration is called E-assess: government agencies use submitted data to assess taxes without the need for tax forms; taxpayers have limited time to check the taxes calculated by the government. Some countries are already reaching this dimension, but at the moment, none is at such an advanced level.

Hungary: Trends and directions

Recently, there have been changes in the evolution of digital taxation in Hungary. The Ministry of Finance and the Tax Authority are not expected to slow down with the digital transformation. The recent formation of the head of the Tax Authority, an IT specialist, shows an even greater commitment to digital tax administration. Due to the pandemic, there has been a shift towards E-audit, although not yet achieved.

By 2021, tax authorities have started preparing VAT returns digitally and Corporate Income tax is being developed. The next step is SAF-T (level 5 of the maturity model), Standard Audit File for Tax, containing all relevant audit data. As already mentioned, some countries are already moving in this direction, Hungary foresees the arrival by 2023.

As the digital world travels rapidly, companies need to be prepared. The future can be described by the digitalization of local taxes as well, which in a way simplifies compliance services. For this to work, all kinds of data must be available to the authorities and stored.

Global minimum tax – An international tax update

At the suggestion of the US, the G7 agreed to introduce a global minimum tax rate of 15%.

Only a few EU countries are affected, including Hungary with a corporate tax rate of 9%. The Hungarian government firmly rejected the idea on sovereignty grounds. In return for supporting the proposal, EU countries have asked for US cooperation on the taxation of multinational companies in the digital economy.

Critics of the proposal claim that standardization of rates alone is ineffective in achieving fair taxation, as several multinationals achieve 0-1% ETR despite top rates of 20% and above. The global minimum tax was not intended as it was presented, the effect was much bigger than expected.

Hungary has the highest level of VAT (27%) and for this reason, 15% might be unreasonable.

What would the 15% tax rate entail?

As a next step, the G20 is likely to support the proposal. It has to be dealt with at the level of the OECD (Organisation for Economic Co-operation and Development), which cannot make binding legislation. It is questionable how to include similar taxes (e.g. local business tax) in a Corporate Income Tax proposal. Overall, no quick action is expected.

What can companies do to set up for tax digitalization?

There are pre-steps for companies to comply with this type of process.

- The first point involves the effective use of data, which is characterized by the following features: clean data, a version of the truth, auditability of data. Auditability means having the necessary data to track what happens, when, and where in the tax area.

- Collaboration with tools, software, and discussions with authorities for the best result. Cooperate with different actors in the ecosystem.

- Focus on the process: make sure you are ready, have contact lists ready and the “Things” fixed first.

- Adaptability: don’t underestimate changes, but know how to move quickly and flexibly.

- From reactive to proactive: reactivity is now synonymous with slowness. Nowadays, you have to understand when things happen, what to do, and be able to act quickly, sometimes even anticipating the problem.

- Art of the Possible: talk to service providers about what new things are available to make you more agile.

Some examples

- Robots as support in taxation: tests were carried out, and bots won against all cases submitted to them.

- Independent software solutions: effective on BUSINESS VAT, WAGE TAXES.

- Platforms: everything in one place. Companies need to realize the usefulness of these tools. Everyone can focus on their section, but you can also have a more complete overview.

- Analysis software: perform the analysis. It works like Excel but is more transparent. It helps to scrutinize the data.

Concerning these solutions, given the continuous digital development, updates are expected to be faster and more frequent. Every business’s challenge is opening its eyes and trying to understand what can be done differently. These changes are coming, and they are increasingly on the agenda, like it or not. The key is to have a proactive approach to these changes and be better prepared.

USEFUL LINKS:

- Impact of Digitalisation on International Tax Matters, European Parliament

- https://www.oecd.org/going-digital/topics/tax/

Recent posts